Introduction

Since Updata first introduced our framework for analyzing SaaS companies, we’ve refined our thinking by evaluating hundreds of potential investments and gaining insight from many CEOs, CFOs and other collaborators. This updated framework, as well as an Excel tool available here, allows others to run their own numbers.

We owe thanks to many others, including Neil Hartz, a co-author of the original document. Please keep the feedback coming!

We believe there are two SaaS metrics that matter most: Gross Margin Payback Period (GMPP) and Return on Customer Acquisition Cost (rCAC). GMPP is the number of months required to break even on the cost of acquiring a customer. rCAC incorporates the element of customer churn/retention into the equation and calculates the multiple of the acquisition cost provided by the lifetime gross profit of a customer. A good SaaS business will have GMPP under 18 months and rCAC above 3x. A great SaaS business will have GMPP and rCAC of less than 12 months and above 5x, respectively.

Perhaps the most underappreciated part of unit economics analysis is the importance of cohorts. GMPP and rCAC offer powerful insights but are often meaningless if calculated only at the company level. Company-wide metrics ignore the fact that most SaaS vendors sell multiple products through a variety of channels and acquire customers over many months, quarters and years. Accordingly, we believe cohort level analysis is necessary and must be run across at least three critical dimensions: Vintage, Product, and Channel. Doing so will allow us to answer important questions such as:

- Vintage: “Are customer payback periods increasing or decreasing?”

- Channel: “Do we get a better ROI from direct sales or from channel sales?”

- Product: “How does customer lifetime value vary by product?”

Please note that this cohort-based unit economics framework is focused on customer-level data and yields completely different insights than can be derived from analyzing GAAP financial statements. These unit economics are more telling than GAAP financials about the health of a business. In fact, this framework is the underpinning of every investment we make in a SaaS or recurring revenue business.

Step 1: Calculate MRR – Monthly Recurring Revenue

MRR is the average monthly recurring revenue per customer. While company-level MRR explains average monthly recurring revenue across the entire customer base, it ignores variability across vintage, channel and product cohorts. For example, different products have different economics – a $300 basic product should not be lumped in with a $1,500 premium offering when assessing MRR. Also, tracking MRR over time within an individual cohort will illuminate upsell/downsell trends – a significant factor in the efficacy of the SaaS business model.

Step 2: Calculate tCAC – Total Customer Acquisition Cost

tCAC is the fully burdened cost required to sign up a new customer, including net one-time onboarding costs. A proper tCAC calculation involves consideration of all departmental costs of sales and marketing, plus one-time costs.

When calculating tCAC, companies often look only at the variable cost of customer acquisition, such as sales commissions and marketing campaign expenses. While this is an appropriate way to calculate the economics of acquiring the next marginal customer, we do not believe it reflects the full cost of customer acquisition – after all, the segmentation work by the product manager, the sales enablement tools, and the CRM system also helped bring in the deal. Variable-only CAC also fails to recognize that fixed costs must scale over time as the company grows, usually in a stair-step function as infrastructure is added.

Including fully burdened department-wide sales and marketing acquisition costs is a good start to calculating tCAC, but doesn’t tell the whole story – don’t forget about the costs of onboarding. These are the onboarding or provisioning processes, such as training and data migration, that are required to light up a new account. Any upfront expense or capex outlay, net of what is billed back to the customer, should be rolled into the onboarding cost and included in tCAC. And by the same logic, tCAC should be reduced by any gross profit derived from onboarding services.

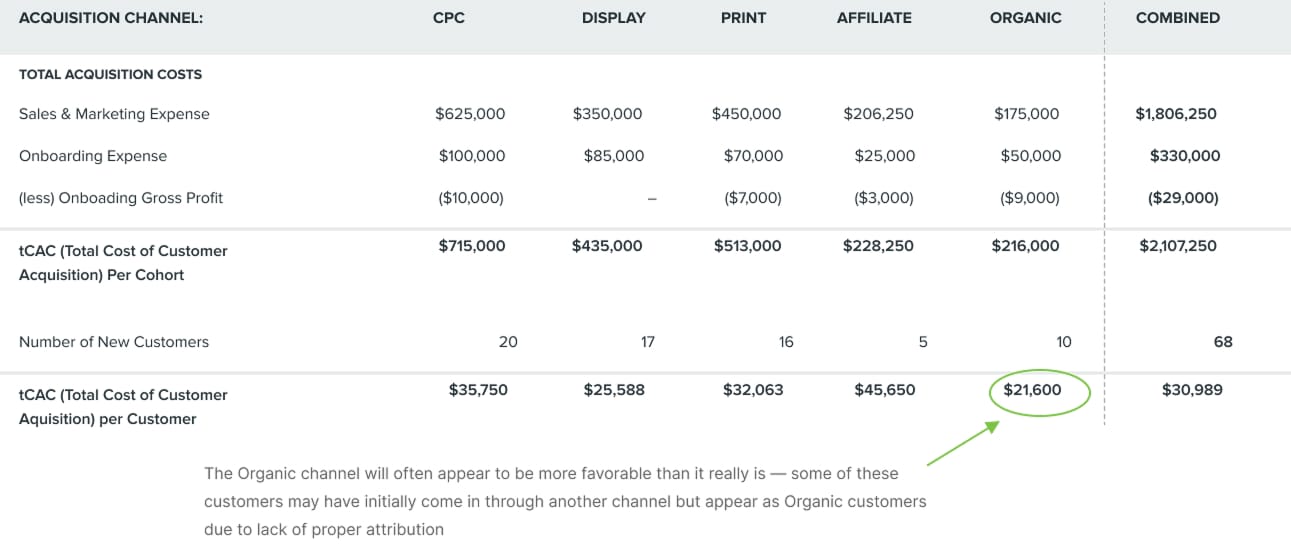

Lastly, tCAC must be reported by cohort in order to properly represent the cost of acquiring specific customers rather than a generalized “average” customer. In Figure 2 we show tCAC by channel.

Two difficulties encountered when isolating tCAC by cohort are attribution and cost allocation. Attribution is difficult, especially in marketing, because spend in one channel often drives the end result in another. For example, a display advertising campaign may generate customer interest that results in a sale through an affiliate channel. These untraceable accounts often fall into the “organic” channel, inflating its apparent efficacy.

The second issue of cost allocation arises because it’s not always clear how to allocate costs between tCAC and recurring COGS. After all, some customers will require extra handholding and attention at the outset of their tenure and some will require constant care during their lifetime to prevent churn. To deal with these ambiguous situations, we recommend keeping it simple, clearly defining assumptions, and being consistent over time.

Note: We recommend matching sales cycle expense to customer acquisition timelines. If a company typically takes three months to move a customer from lead to close, then we should consider expenses from three months prior to determine tCAC.

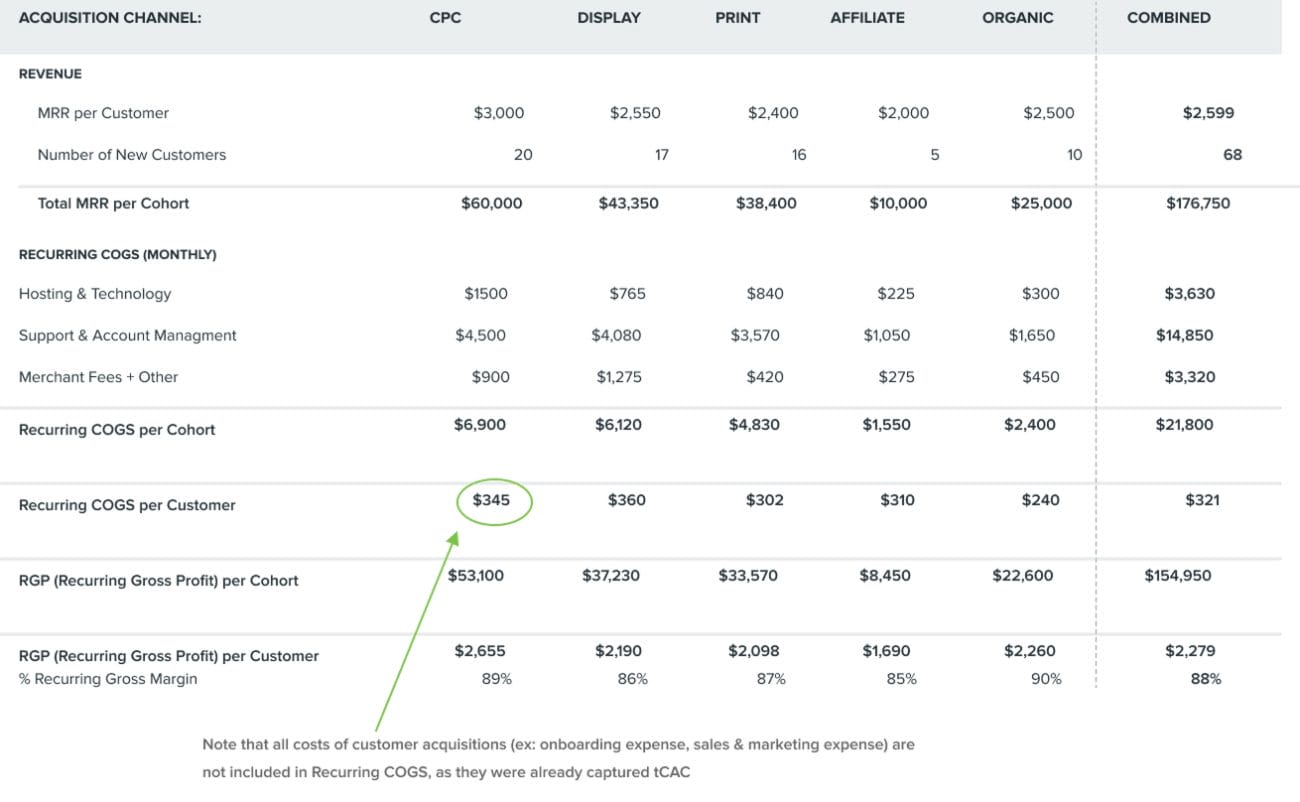

Step 3: Calculate RGP – Recurring Gross Profit

RGP is the gross profit generated each month by a customer (RGP = MRR – recurring COGS). Typical recurring COGS items include the cost of customer delivery (e.g., datacenter usage), the cost to support the customer (e.g., call centers) and payments to 3rd parties (e.g., software license fees).

The key to properly calculating recurring COGS, and consequently RGP, is to include all month-to-month costs required to maintain a customer that is already live on the software, but to exclude the initial expenses necessary to light up a new customer; those one-time expenses were captured in tCAC. There will be a mixture of fixed COGS (e.g., servers) and variable COGS (e.g., merchant fees) captured in this bucket of costs.

Note: A common mistake is to use revenue rather than gross profit to measure customer payback. Using revenue fails to account for the true costs of supporting a customer and can lead to faulty conclusions about unit economics.

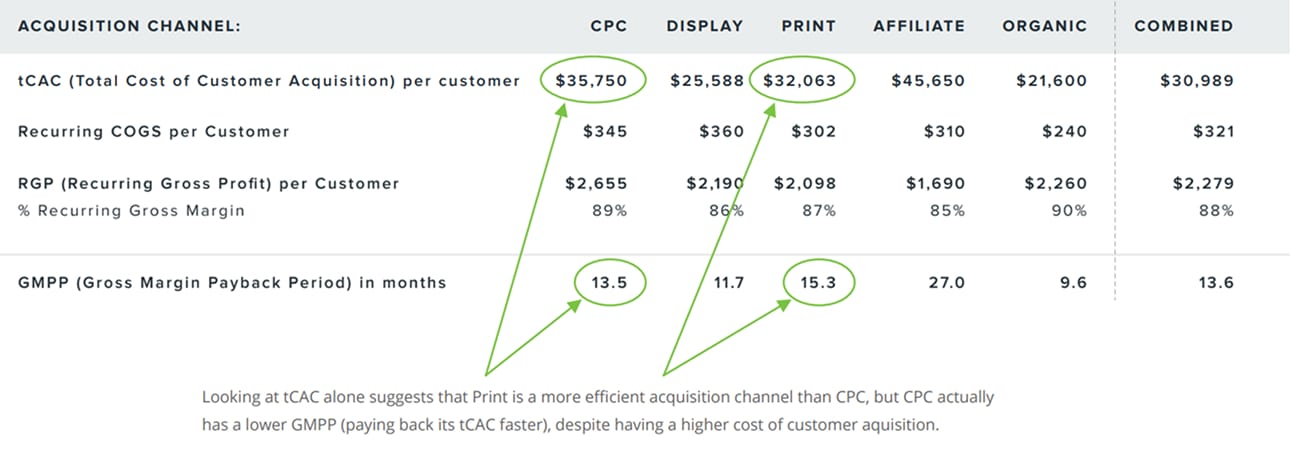

Step 4: Calculate GMPP – Gross Margin Payback Period

GMPP is the number of months required to break even on the cost of acquiring a customer (GMPP = tCAC / RGP). GMPP is fundamentally an indicator of the working capital needs of the business. Shorter is better because the time to recoup customer acquisition costs should be as quick as possible. Using GMPP to compare cohorts is one of the first levels of analysis that pulls multiple metrics together to derive actionable insight.

Note: RGP does not confirm to GAAP accounting and neither do many of the metrics in this paper. Instead we are trying to focus on the intrinsic unit-level economics. For example, we include onetime costs such as onboarding in tCAC, but they would likely fall under COGS and GAAP accounting. Items that are typically capitalized and then depreciated over their lifetime, such as devices shipped to the consumer, are instead recognized as an upfront expense in our framework.

Note: GMPP offers insight into the intrinsic capital efficiency of the business. Oftentimes, customers pay in advance, as in the common “annual subscription, paid upfront” arrangement. Rather then focusing on GAAP revenue recognition, operators should focus on cash (i.e. billings-based) payback periods, as upfront payments are an effective way to finance growth.

Before jumping to conclusions about marketing budget reallocations, however, it’s important for high-growth SaaS businesses to realize that acquisition channels are not perfectly elastic. Channels that appear scalable at 100 monthly additions with rapid GMPP may not scale with consistent efficiency to 1,000 monthly additions. For example, CPC campaigns that work at low volumes can become prohibitively expensive at high volumes due to finite online inventory. Having said that, we are enthusiastic advocates of A/B testing, new channel development, and data-driven searches for incremental gains. Armed with this cohort level analysis, SaaS companies have a better chance at getting closer to the elusive efficient frontier of channel mix.

Note: For simplicity in our example we are assuming nominal cash flows, but in reality the future cash flows should be discounted for the time value of money. This factor has a compounding effect on churn, a metric we will explore in the next section.

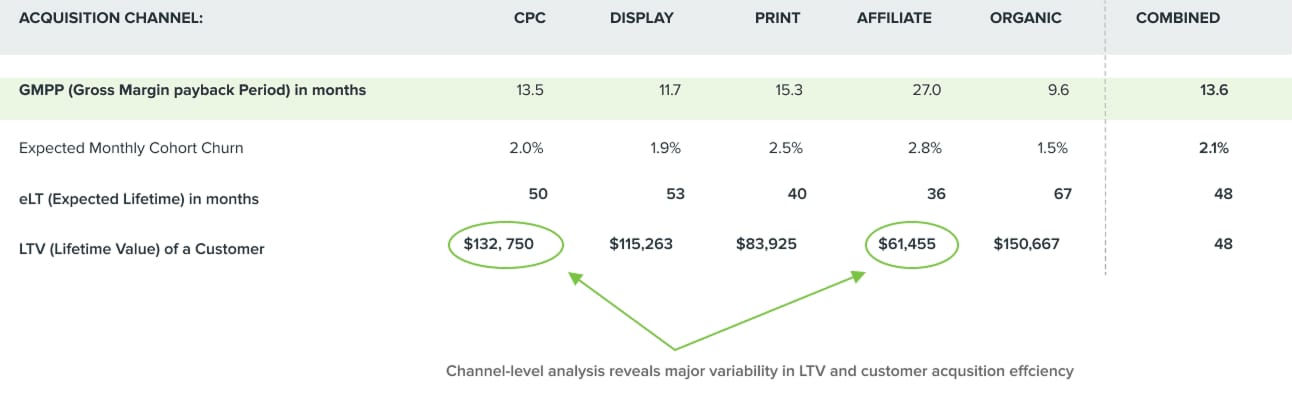

Step 5: Calculate eLT – Expected Lifetime

eLT is the length of time that a company expects to keep a paying customer (eLT = 1/Churn). While some customers will churn out immediately and others will stick around for an eternity, eLT is concerned with the average lifetime across a cohort of customers. SaaS companies often have long-term contracts that suggest a predetermined minimum customer life, but we care more about innate customer “stickiness,” not contract length. After all, contracts can be renewed – and broken.

Note: We recommend cutting off eLT at five years because (1) the true value of “out year” cash flows are significantly impacted by the time value of money, and (2) it’s very hard to predict customer churn behavior five years in the future.

Keep in mind that dollar churn is more important than account churn. While SaaS companies will constantly be fighting a losing battle against account churn (at best, breakeven), customers who stick around often increase the size of their subscription over time. Account growth can occur through price increases, seat license growth, or the purchase of additional modules.

Churn itself is a much deeper concept that we explore in a separate white paper here, and indeed most retention curves are more complex than our simplification suggests. Churn is a tricky topic that can be easily misconstrued or gamed to tell a certain story …is it monthly or annual? Logo or dollar? Gross or net? Cohort or company-wide? Thus, we discourage thinking about churn as a single number and believe instead that eLT and detailed retention curves by cohort provide the best insight into customer behavior.

Step 6: Calculate LTV – Lifetime Value

LTV is the economic value, net of costs, delivered over the life of a customer, and is equal to lifetime gross profit (LTV = RGP x eLT). While GMPP is a great tool for comparing the efficiency of different cohorts from a time-to-payback perspective, LTV takes it one step further by incorporating expected lifetime. As previously noted, we encourage cutting off customer lifetimes at five years for conservatism.

After repaying the fully burdened cost to acquire a customer and any variable recurring costs required to support the customer, LTV goes towards paying off the remaining fixed costs in the business – G&A and R&D – where significant operating leverage can be found with scale.

Step 7: Calculate rCAC – Return on Total Customer Acquisition Spending

rCAC is the multiple of acquisition cost provided by a customer’s lifetime gross profit (rCAC = LTV / tCAC). rCAC provides a churn-adjusted view of unit economics by combining GMPP with expected customer lifetime. In conventional terms, this is the ROI on the spend to acquire a customer – perhaps the most important thing to know when analyzing a business model.

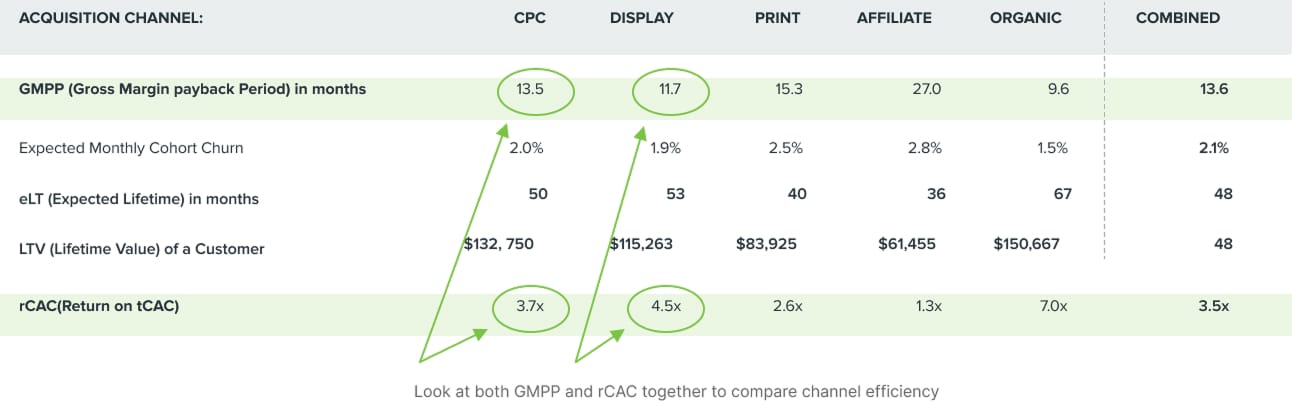

By utilizing GMPP and rCAC together, we can determine the time required to recoup the cost of acquiring a customer and the expected return on acquisition spend. The two metrics together are crucial when making decisions about the most efficient ways to allocate resources. A cohort with a rapid GMPP but low rCAC ultimately means little profit will be realized from customers because they churn soon after the breakeven point. Conversely, a cohort with great rCAC but very long GMPP creates a substantial need for capital to weather the storm until it becomes profitable.

Applying the Framework

A few rules of thumb help put the framework into action. A GMPP under 12 months is great; a GMPP up to about 18 months is acceptable. After 18 months, however, the present value of those cash flows way out in the future is harder to justify against the upfront acquisition expense. For example, a GMPP of 36 months suggests that three years are required to break even on the customer acquisition cost. So if monthly churn for that cohort is just 3%, these customers will never be profitable because their lifetime is only 33.3 months against a 36 month payback period; operators should redirect resources away from cohorts displaying this sub-par performance. Alternatively, a GMPP of 12 months or less indicates tCAC is repaid within a year. Assuming manageable churn, a company with such a short GMPP should be throwing fuel on the fire and investing in efficient growth.

For rCAC benchmarks we like to see a return of at least 3x, with 5x and above being top of the class. rCAC below 3x doesn’t leave much to cover operational expenses beyond the acquisition expense and recurring COGS. Low rCAC means a company earns little over the life of each customer and new customers have to be added quickly just to replace ones that churn. Higher rCAC, on the other hand, provides more headroom to cover expenses and reinvestment. Ultimately, realizing multiples of tCAC is how SaaS companies build enterprise value.

Turning to our example, we only have one non-organic acquisition channel with passing economics – the Display channel with a GMPP of 11.7 months and an rCAC of 4.5x. As is often the case, the organic channel has superior economics, but it’s hard to “invest” in this type of customer acquisition.

We hope entrepreneurs find this updated framework useful for analyzing the unit economics of their SaaS businesses. Please see our Excel worksheet here to get started.